AI & ENGINEERING

Why the $340k internal portal is now a two-day build, and what that means for the consulting industry.

A mid-market manufacturing company I know got a quote last year to build an internal portal. Nothing exotic: a dashboard for their ops team, a couple of forms for vendor onboarding, single sign-on against their existing identity provider. The quote came in at $340,000 and an eight-month timeline from a name-brand systems integrator. They paid it. The portal shipped two months late, was already obsolete by the time it landed, and is currently being rebuilt by two of their own engineers using Claude Code and Retool inside a single 40-hour week.

That story isn’t unusual. It isn’t the whole market, but it captures a pattern now appearing across routine internal tooling: the software is getting cheaper, while the old delivery model still prices it like custom infrastructure.

The Distinction That Matters

When people say “middleware is dying,” they’re usually wrong about the noun. Architectural middleware isn’t dying. It’s metastasizing into AI gateways, semantic routers, and what CIO Magazine has started calling “mindware” (intelligence embedded directly in the data-integration layer). The market for middleware-as-software is growing fast. Doss just raised $55 million to put intelligence inside ERP. The plumbing layer is more alive than it’s been in fifteen years.

What’s dying is the labor market that grew up around building and integrating that plumbing. The premium-margin consulting engagement to “stand up a portal that talks to SAP” is collapsing on a timeline that should terrify anyone whose firm depends on it.

Call it the middleware tax. It’s the structural surcharge a generation of dev leaders has paid to systems integrators to translate between their business and their software. The middleware itself was always cheap; the translators were expensive. For two decades the translators captured most of the value because building anything was hard, slow, and required a particular kind of headcount that most companies couldn’t justify hiring full-time.

That math has changed. The collapse isn’t because integrations disappeared. It’s because four cost centers compressed at once: requirements translation, boilerplate implementation, UI scaffolding, and first-pass QA. The expensive part used to be moving from business intent to working software; AI-assisted tooling turns that into a review-and-governance problem rather than a blank-page delivery problem. The translators know it. They’re now restructuring around it in real time, in public, with a candor that should tell you everything you need to know about the trajectory.

The Numbers Are Already Here

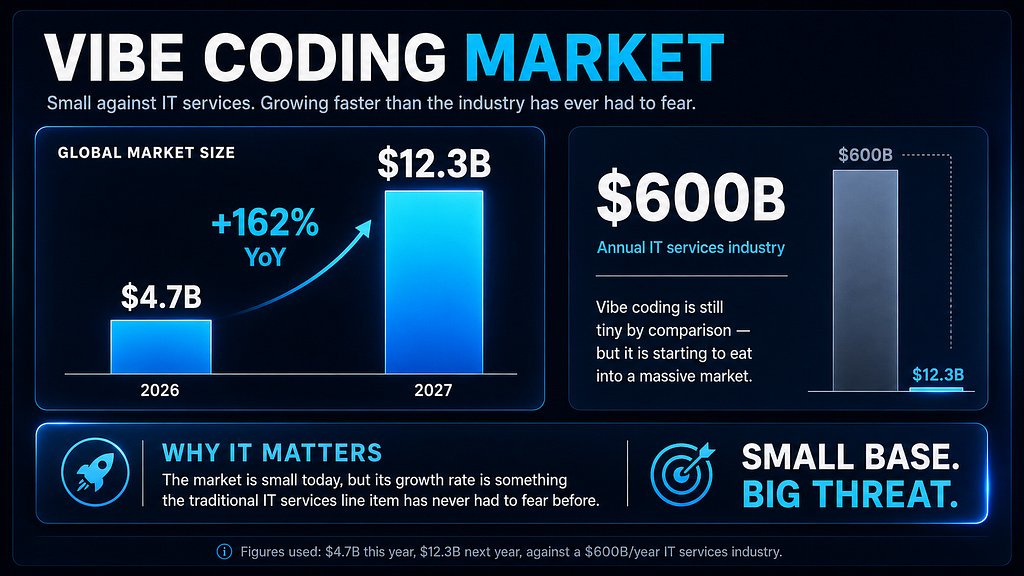

Ninety-two percent of US developers now use AI coding tools daily, and that same survey puts AI-generated code at forty-one percent of all code. GitHub’s Copilot data runs higher, closer to forty-six percent among its active users. The vibe coding market is $4.7 billion this year and projected at $12.3 billion next year. That’s small against the $600-billion-a-year IT services industry it’s starting to eat, but it’s growing at a rate that line item has never had to fear before.

Andrej Karpathy, the engineer behind Tesla’s Autopilot who later coined “vibe coding,” has already evolved past it: he now calls the discipline “agentic engineering,” because you’re not writing the code directly ninety-nine percent of the time. You’re orchestrating agents who do. That shift, from typing code to supervising agents that type code, is what’s eating the bottom of the consulting pyramid.

Look at the response from the firms that have the most to lose.

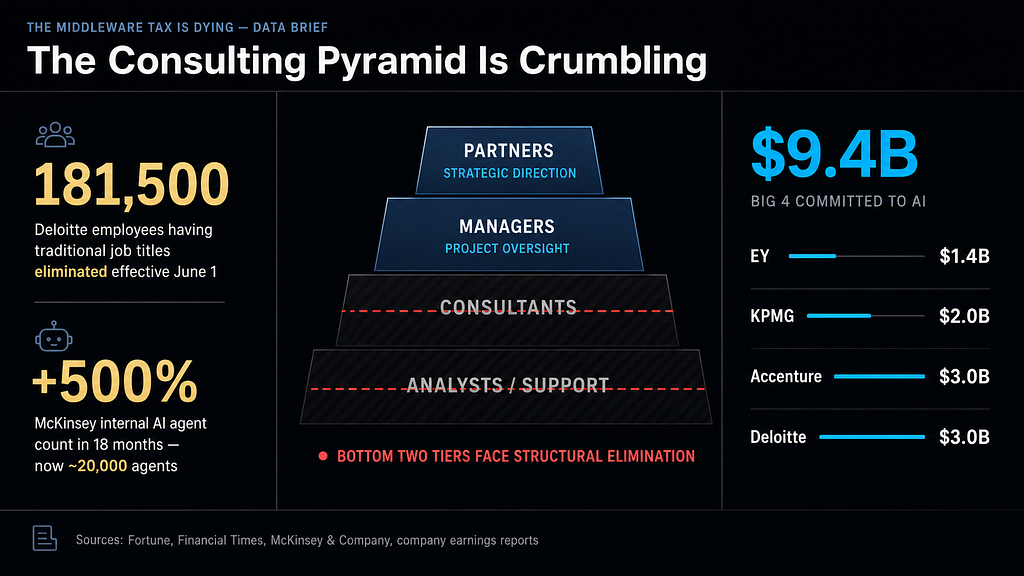

Deloitte announced in January that it is overhauling traditional job titles for 181,500 US employees effective June 1, a move widely framed as part of the firm’s AI-era modernization. Read the official framing carefully: the pyramid model, in which large teams of junior consultants handle time-intensive tasks while partners oversee and bill, faces structural pressure when AI agents can perform much of that junior work. McKinsey grew its internal AI agent count by five hundred percent in eighteen months, to roughly twenty thousand agents. The Big 4 collectively committed over $9.4 billion to AI in the same window: EY put up $1.4 billion, KPMG $2 billion, Accenture and Deloitte $3 billion each.

The consultancies aren’t investing $9.4 billion to keep the same org structure. They’re investing to replace the bottom of their own pyramid. They’ve correctly identified that the junior rungs, the people who used to do the time-intensive translation work, are being absorbed by software they themselves are racing to own. They’d prefer to be the new middleware layer than be disrupted by it. The Deloitte title overhaul isn’t a tangent to that spend; it’s the same decision viewed from the headcount side. Whether the pivot works is the most expensive open question in the services economy.

Gartner predicts that by 2026, eighty percent of low-code platform users will come from non-IT departments and eighty percent of enterprise APIs will be at least partially machine-generated or adaptive. That’s not a forecast about cost reduction. It’s a forecast about who’s building. The people who used to wait three quarters for IT to deliver a tool are now building the tool themselves before the procurement cycle closes.

If you want a single document that captures the shift, the Stanford Digital Economy Lab published an Enterprise AI Playbook in March based on fifty-one successful enterprise deployments. The case studies aren’t theoretical. They’re companies your peers compete with, building tools at speeds your procurement department doesn’t believe are possible until someone shows them the working software.

The Counter-Arguments You’re About to Make

You’re going to want to push back on this. Here are the five responses worth taking seriously and the honest answer to each.

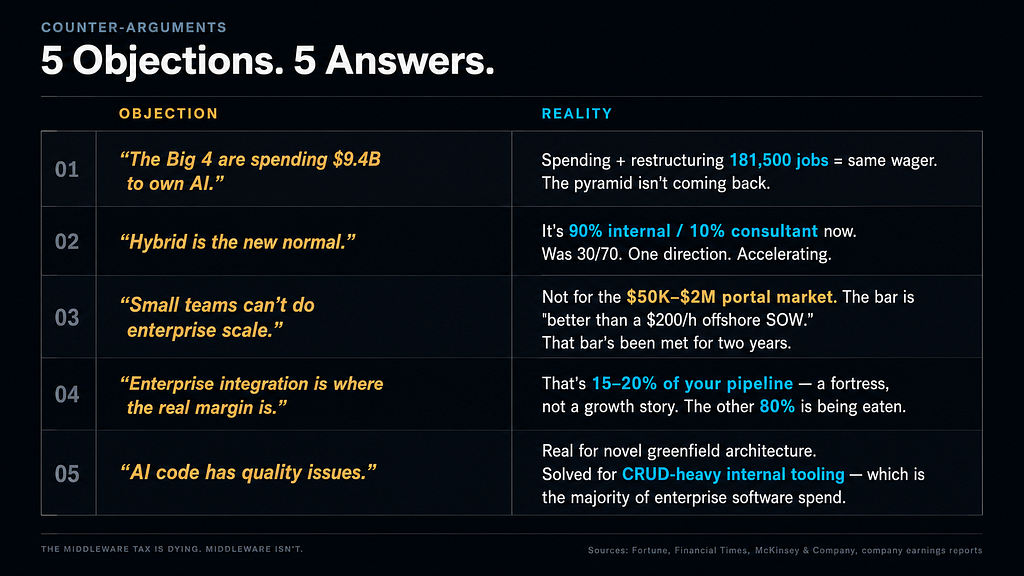

The Big 4 are spending $9.4 billion to own this. Yes, and they’re also restructuring 181,500 job titles to absorb the impact. Spending and restructuring aren’t contradictory; they’re two sides of the same wager. The wager may pay off. It won’t bring back the pyramid model.

Hybrid is the new normal. True today. The hybrid mix is also shifting one direction: five years ago a typical enterprise project was thirty percent internal and seventy percent consultant. The current ratio at well-run mid-market companies is closer to ninety/ten. The direction is one-way and it’s accelerating, not stabilizing.

Small teams can’t do enterprise scale. True for some enterprise scale. Not true for the fifty-thousand-to-two-million-dollar internal portal market where consultancies have been printing money for fifteen years. The bar isn’t “perfect code.” It’s “better than what a $200-an-hour offshored team ships under a fixed-bid SOW.” That bar has been met for two years.

Enterprise integration is where the real margin is anyway. Correct, and if multi-vendor enterprise integration is fifteen to twenty percent of your pipeline, you’ve correctly identified your fortress. The other eighty percent is still being eaten. A fortress is a good thing to have. It’s not the same as a growing business.

AI code has quality issues. Real concern, and the honest answer is that the risk profile varies by workload. For CRUD-heavy internal tools with strong templates, review, tests, and deployment guardrails, AI-assisted development is often good enough to compress cost and timeline. For novel architecture, security-sensitive systems, and unclear ownership models, the risks remain material. The portals, the dashboards, the form-driven workflows, the reporting layers are the most boring code in the world, which makes them the work AI tooling is best suited to, provided the guardrails are real.

Where This Works (and Where It Doesn’t)

The thesis is strongest for net-new internal tooling at SMB and mid-market companies. Greenfield portals, dashboards, reporting layers, internal CRMs, ops workflows, vendor onboarding flows, anything where the spec is “give my ops team a button that does X.” If you’re in that lane and you’re still hiring a name-brand SI to deliver it, you’re paying the middleware tax and you’re paying it for no structural reason.

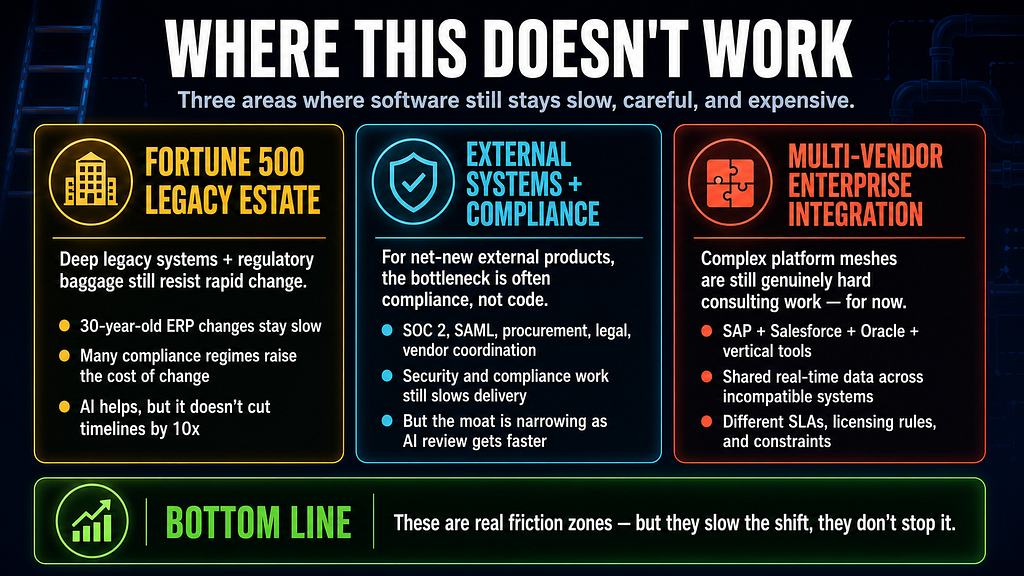

The thesis is weaker for three specific cases that deserve naming.

Fortune 500 with deep legacy estate and regulatory baggage. Modifying a thirty-year-old ERP that touches twelve compliance regimes is still slow, careful, expensive work. The AI tooling helps. It doesn’t collapse the timeline by a factor of ten.

Net-new external-facing systems with security and compliance scope. Here’s the honest version of the counter the Big 4 will reach for first. Compliance scope is real, and it doesn’t vanish because the code got cheap. The blocker on external integrations is rarely the code; it’s the SOC 2 review, the SAML configuration, the vendor cooperation requirements, the procurement cycle, the legal sign-off. But compliance slows the timeline; it does not prevent it, and the slowdown is itself shrinking. AI-assisted security and compliance review is already moving faster than the eighteen-month norm, which means the moat is getting narrower every quarter, not wider.

Multi-vendor enterprise integration. SAP plus Salesforce plus Oracle plus three vertical-specific platforms, all needing to share a customer record in real time, all governed by different SLAs and licensing constraints. Genuinely hard. Genuinely still consulting work, for now.

So the honest framing is this: the middleware tax is dying fastest in the segment where it should never have existed in the first place, which is the part of enterprise software that’s functionally an internal admin tool with company-specific business logic on top. That segment represents a large, high-margin portion of the work many consultancies have historically packaged as custom digital transformation. The remaining work, the genuinely hard stuff, will be done by smaller, more specialized firms or by hybrid models where the consultant is an architecture and governance partner rather than a labor arbitrage vendor.

What To Hire For Instead

If you’re a dev leader staffing for the next eighteen months, the changing math isn’t subtle. Hire one senior engineer who’s fluent in AI tooling and product thinking before you hire two mid-level engineers who aren’t. Hire a product manager who can write a tight spec before you hire a project manager who can run a status meeting. Pay a Retool or a Tooljet license instead of a six-figure portal SOW. Build an internal pattern library, even an informal one, so that the work your AI tooling produces converges on shared conventions instead of becoming a new flavor of legacy chaos. Keep a relationship with a small specialist partner for the work that genuinely warrants outside expertise; stop putting your routine internal builds out to tender.

One discipline keeps the speed safe rather than reckless. If a build is mostly forms, dashboards, approvals, reporting, and role-based workflow, do it internally with AI-assisted tools and senior oversight; if it touches regulated customer data, multi-vendor state synchronization, revenue-critical workflows, or legacy ERP mutation, bring in a specialist. And whatever you ship fast, ship it accountable: clear ownership, access control, logging, test coverage, CI/CD, secrets management, and a named person responsible for support. Speed without those isn’t speed; it’s deferred cost.

The companies that figure this out in the next twelve months are going to ship more software than their competitors at a fraction of the headcount and budget. The companies that don’t are going to keep paying the middleware tax and wondering why the faster firms keep lapping them. This isn’t a ten-year tide you can wait out. It’s a twelve-month one you’re either ahead of or behind.

The middleware tax is dying. Middleware isn’t. The two have always been separable. The only thing that’s changed is that you can finally tell them apart.

Sources

- State of Vibe Coding 2026 (taskade) (AI-tool adoption + market size)

- Deloitte to scrap traditional job titles as AI reshapes the Big Four (Fortune)

- Vibe coding is passé: Karpathy’s “agentic engineering” (The New Stack)

- Engineering the AI-ready enterprise: from middleware to mindware (CIO)

- The Enterprise AI Playbook: Lessons from 51 Deployments (Stanford Digital Economy Lab)

- Echelon’s AI agents take aim at Accenture and Deloitte (VentureBeat)

Tags: Artificial Intelligence, Software Development, Consulting, Vibe Coding, Enterprise Software