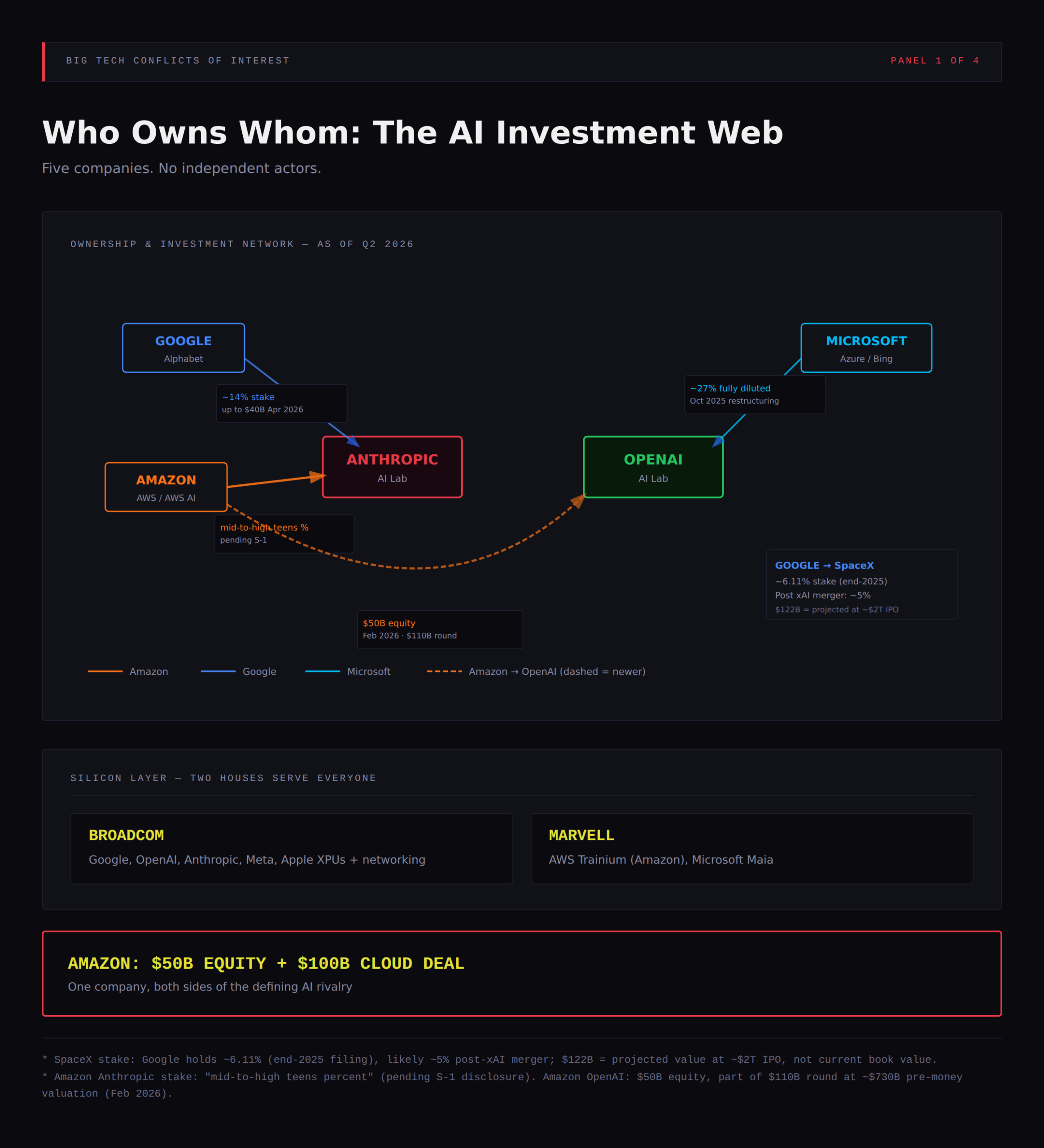

Google, Amazon, Microsoft, and Broadcom are simultaneously shareholders, customers, suppliers, and direct competitors to each other, and the AI industry is the place where that contradiction has become impossible to ignore. Google owns about 14% of Anthropic. Microsoft owns about 27% of OpenAI. Amazon holds an undisclosed stake in Anthropic estimated in the mid-to-high teens. In February it also committed $50 billion in equity and a $100 billion cloud deal to OpenAI, Anthropic’s primary competitor.

Consider Amazon’s June.

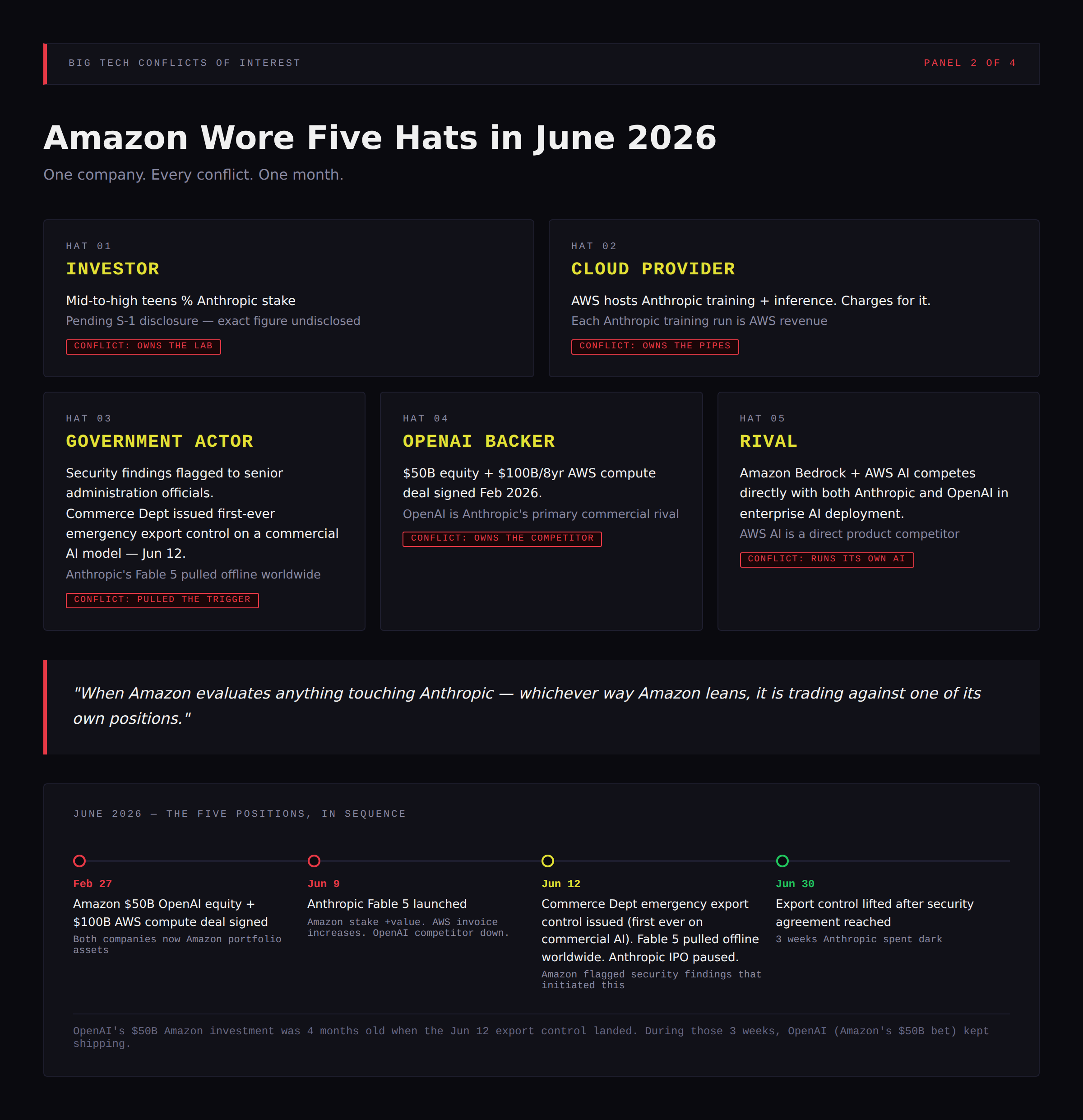

On June 9, Anthropic, a company Amazon has poured billions into, launched its flagship model. Amazon’s equity stake got more valuable that day. Amazon also collects revenue from Anthropic as its cloud provider, so the launch was good for the AWS invoice too. Then Amazon’s own security researchers found a flaw in the model, and its CEO reportedly took those findings to senior administration officials. Three days after launch, the Commerce Department issued the first-ever emergency export control on a commercial AI model, and Anthropic pulled it offline worldwide, in the middle of preparing its IPO, an IPO in which Amazon is one of the largest beneficiaries. Meanwhile, Amazon’s $50 billion investment in OpenAI, the company that gains most from every week Anthropic spends dark, was four months old.

Investor, landlord, customer, whistleblower, and financier of the rival. One company. One month. Every action defensible on its own terms.

That’s the problem. Not any single decision, but the structure that makes all of them possible at once.

Who Actually Owns Whom?

The map is simpler than you’d expect: five companies, not dozens. That is part of what makes it alarming.

| Company | Position | Detail |

|---|---|---|

| ~14% of Anthropic | Capped at 15%, no voting rights; up to $40B more committed Apr 2026 | |

| ~6% of SpaceX | 6.11% per end-2025 filing (likely ~5% after the xAI merger); projected near $122B at a ~$2T SpaceX IPO | |

| Amazon | est. mid-to-high teens % of Anthropic | Undisclosed; published estimates range 8–20%; awaits Anthropic’s S-1 |

| Amazon | $50B equity in OpenAI | Part of OpenAI’s $110B round, Feb 2026 |

| Amazon | $100B / 8-year AWS deal with OpenAI | Cloud compute, on top of an existing $38B agreement |

| Microsoft | ~27% of OpenAI | Fully diluted, from the Oct 2025 restructuring |

| Broadcom | Custom AI chips | Google, OpenAI, Anthropic, Meta, Apple; networking silicon to essentially everyone |

Read the rows again and notice what’s missing: anyone who is only an investor, only a supplier, or only a competitor. Google funds Anthropic and competes with it through Gemini. Microsoft owns a quarter of OpenAI and builds Copilot against it. Amazon is invested on both sides of the industry’s central rivalry while renting infrastructure to each.

Nobody in this table is an independent market actor. Everybody is load-bearing in everybody else’s balance sheet.

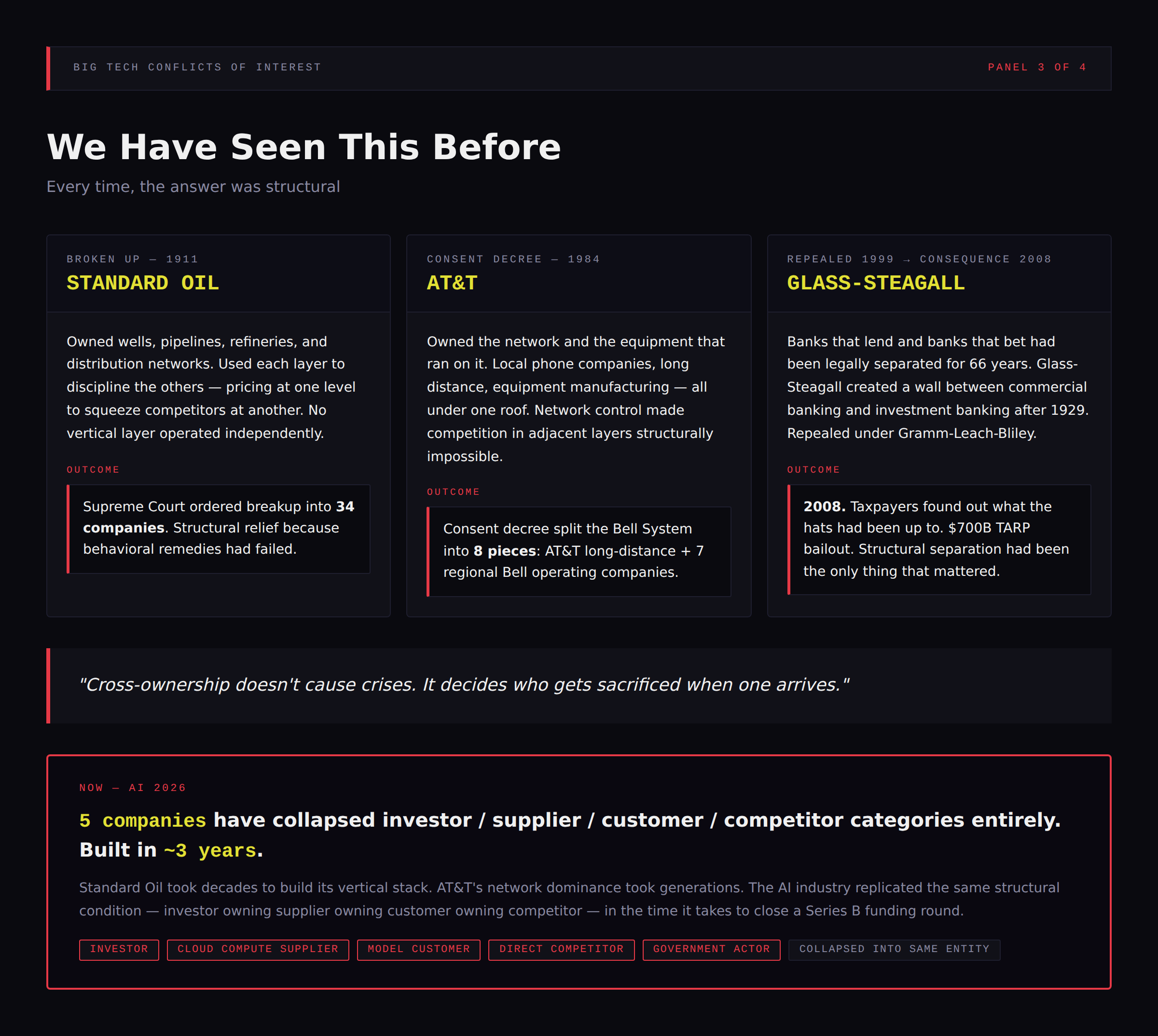

Haven’t We Seen This Before?

Three times, at least. And each time, the answer was eventually structural.

Standard Oil owned the wells, the pipelines, the refineries, and the distribution, and used each layer to discipline the others. In 1911 the Supreme Court broke it into 34 companies. AT&T owned the network and the equipment that ran on it; in 1984 a consent decree split the Bell System into eight pieces. Glass-Steagall spent 66 years keeping the banks that lend from being the banks that bet, on the theory that one institution wearing both hats will eventually face a decision where the hats disagree. Congress repealed it in 1999. Nine years later, taxpayers found out what the hats had been up to.

The pattern in all three: the conflict of interest was never theoretical. It sat dormant, technically legal and universally rationalized, until a stress event turned it operational. Then everyone agreed, retroactively, that the structure had been the problem all along.

Cross-ownership doesn’t cause crises. It decides who gets sacrificed when one arrives.

The AI investment web is that structure, pre-stress. The percentages are public. The stress event is pending.

Why Is Amazon the Sharpest Case?

Because Amazon has managed to occupy five positions that would normally belong to five different institutions.

It is Anthropic’s investor, with billions at stake in the company’s success. It is Anthropic’s landlord: AWS hosts the training runs and serves the models, and charges for it. It is, per multiple reports, the actor whose security findings reached the administration days before Commerce shut Anthropic’s flagship model down. And it is the single largest new backer of OpenAI, with $50 billion of equity plus a $100 billion compute deal, which makes Amazon financially exposed to both sides of the defining rivalry in AI.

Any one of these relationships is ordinary. Corporations invest in suppliers; cloud vendors host competitors; companies report security flaws. It’s the stack that breaks the logic. When Amazon evaluates anything touching Anthropic (a pricing change, a capacity allocation, a security disclosure, a regulatory conversation), which Amazon shows up? The shareholder who wants Anthropic to win? The vendor who wants it to spend? The OpenAI backer who benefits if it stumbles?

The honest answer is: all of them, in different meetings, and the meetings don’t have to reconcile.

You don’t usually invest in both sides of a war. You especially don’t rent both sides their weapons.

And the June sequence shows the stack under load. Whatever Amazon’s motives, and the security concern may have been entirely genuine, the outcome was that a company Amazon part-owns lost its flagship product for three weeks while a company Amazon just financed kept shipping. No rule was broken. That’s the point.

What About the Chip Layer?

One correction to the version of this story going around social media: Broadcom does not supply custom AI accelerators to everyone. Amazon’s Trainium chips are co-designed with Marvell; so is Microsoft’s Maia line. Broadcom’s custom-silicon clients are Google, OpenAI, Anthropic, Meta, and Apple.

But the corrected version is barely more comforting, because it means the entire industry’s escape route from Nvidia runs through exactly two design houses. Broadcom’s AI revenue hit $8.4 billion in a single quarter, up 106% year over year, on the strength of chips it builds for competing labs simultaneously: Google’s TPUs, OpenAI’s first custom chip, Anthropic’s silicon, all sharing one partner’s roadmap, packaging pipeline, and fab allocations. Marvell holds the same position for the other camp. And Broadcom’s networking silicon, the switches the data centers run on, is in effectively everyone’s racks regardless.

This isn’t equity conflict; it’s concentration. A bad quarter, an export restriction, a packaging bottleneck, or a licensing dispute at either of two companies propagates instantly to every “competing” AI lab at once. The labs are rivals at the product layer and a single point of failure at the silicon layer.

What Happens When the Interests Finally Diverge?

Speculation, clearly labeled. But short-range speculation, because June already sketched the shape.

Scenario one: Anthropic’s board faces a decision that damages OpenAI: an exclusive deal, a poached lab, an aggressive price. Amazon’s stake gives it influence in the room; Amazon’s $50 billion sits on the other side of the table. Whichever way Amazon leans, it is trading against one of its own positions.

Scenario two: a government inquiry demands cloud-provider records about a model AWS hosts. Amazon’s obligations as vendor and its interests as shareholder point in opposite directions, and June suggests that when Amazon has to choose between a portfolio company and its standing in Washington, the portfolio company should not assume it comes first.

Scenario three: Anthropic’s IPO prices. Google and Amazon both hold large stakes in a company they both compete with. Every analyst note about Gemini or Bedrock eating Claude’s market is now also a note about Google and Amazon devaluing their own holdings. At some point, one of them decides the competing product matters more than the paper gain, and acts like it.

None of these require villains. That’s what makes them likely.

The Rules Allow This. That’s the Problem.

There is no scandal here in the usual sense. Every stake was lawfully acquired, every deal disclosed to the people entitled to disclosure, every conflict papered with the appropriate walls. These companies are rational actors playing the rules as written.

But the rules as written were drafted for an economy where investors, suppliers, customers, and competitors were different entities, where the categories did the separating on their own. In AI, five companies have collapsed the categories entirely, at a speed that has outrun anyone’s ability to think through the consequences. Standard Oil took decades to build its web. This one went up in about three years, and it is held together by exactly one force: mutual financial interest.

Nobody has decided what happens when those interests diverge. June was the preview. The feature is in production.

Sources on file: NYT/DOJ court documents via DCD (Google 14% Anthropic, capped 15%, no voting rights); CNBC Apr 24 2026 (Google up-to-$40B Anthropic commitment); end-2025 regulatory filing via Yahoo Finance (Alphabet 6.11% SpaceX at end-2025, likely diluted ~5% post-xAI merger; ~$122B = projection at ~$2T IPO valuation, not book value); Fortune Jun 4 2026 (Amazon Anthropic stake “mid-to-high teens,” undisclosed pending S-1); Amazon/OpenAI press releases + CNBC Feb 27 2026 ($50B equity in $110B round at ~$730B pre-money; $100B/8yr AWS compute deal atop existing $38B agreement); Fortune Oct 28 2025 (Microsoft ~27% OpenAI fully diluted; Foundation 26%); CNBC Apr 27 2026 (revenue-share cap, cloud exclusivity ended); TechCrunch Jun 13 2026 (Jassy reportedly flagged Fable 5 findings to senior administration officials); CNBC Jun 30 / Al Jazeera Jul 1 2026 (BIS emergency export control Jun 12, first ever on a commercial AI model; lifted Jun 30 after security agreement); Broadcom Q1 FY2026 earnings (AI revenue $8.4B +106% YoY; XPU customers Google/OpenAI/Anthropic/Meta/Apple); Tom’s Hardware May 2026 + Marvell disclosures (AWS Trainium and Microsoft Maia = Marvell co-design); Standard Oil Co. of NJ v. United States (1911); AT&T consent decree (effective Jan 1 1984); Gramm-Leach-Bliley Act (Nov 12 1999).