Dead Internet Theory isn’t a conspiracy theory. It’s a supply chain.

In 2025, Sherwood News reported a thing that, if you read it the wrong way, sounds boring.

X (the platform formerly known as Twitter) was paying creators through its monetization program. Many of those creators were posting AI-generated content. Some of that content was attracting engagement from other AI-generated accounts.

The platform was paying the people producing the slop. The slop was being watched, mostly, by other slop. The platform was selling the engagement metric to advertisers.

This is a closed loop.

It’s also not a conspiracy. Nobody had to plan it.

If you’ve spent any time with the Dead Internet Theory, the half-meme, half-grievance idea that the internet has been overrun by bots and the humans are quietly drowning, you know the strong version of the theory assumes a single coordinator. Some agency, some company, some shadowy room of people pulling levers behind the curtain.

That’s not what the documentation shows.

What the documentation shows is a market. A four-tier service economy that has existed in some form for more than a decade, and that, between roughly 2022 and 2025, picked up a new ingredient: generative AI made the cost of producing the content portion of the work go to zero.

The amplification labor was always cheap. The content production was the bottleneck. That bottleneck broke.

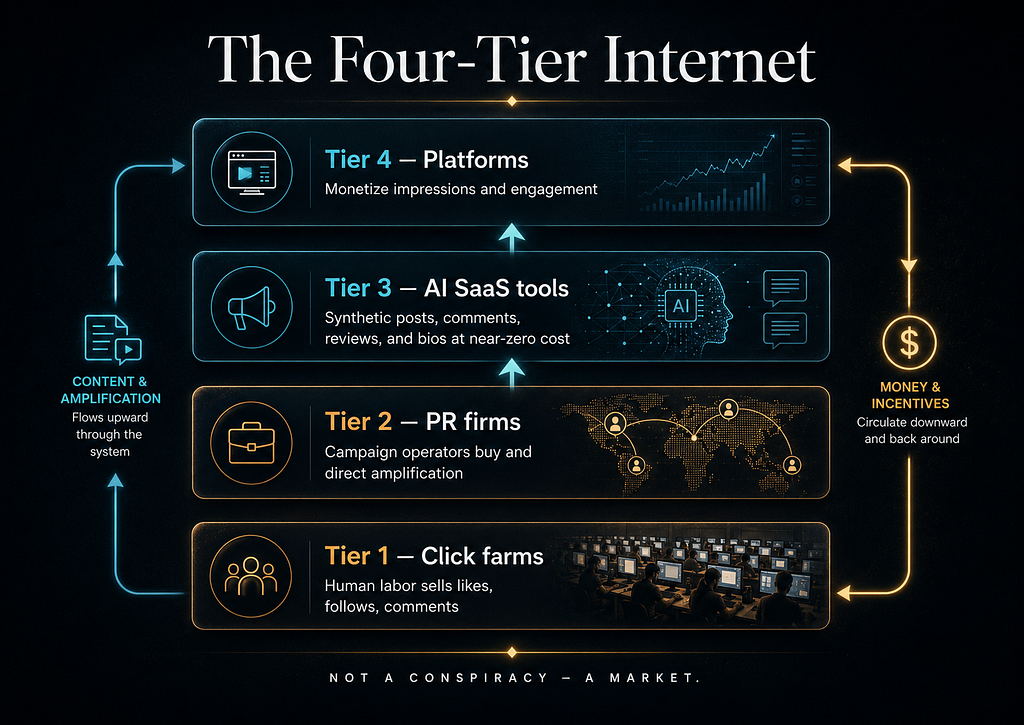

What’s left is an industry with four named layers. Each layer sells something different. Each layer has different customers. Each layer has its own regulatory exposure and its own legal vocabulary. The layers benefit from each other without coordinating with each other.

The bottom is where the people are. Then the PR firms. Then the SaaS tools. Then the platforms themselves.

By the time we get to the tip of the iceberg, the shape of the thing will be clear, and the question the strong-version conspiracy was trying to ask, whose internet is this now, will have an answer that’s harder to sit with than the conspiracy version. Because the conspiracy version has a villain you can name.

This version doesn’t.

Tier 1: The Rooms Full of Phones

In 2023, a British photographer named Jack Latham published a book called Beggar’s Honey. It’s a photo project. The photos are of click farms in Vietnam. Rooms of phones, mounted in wooden frames, each one logged into a social media account, each one tapping out likes and follows and short comments on a rotation.

One operator runs between fifty and four hundred devices through specialized software. The work is paid per action. A like is worth a fraction of a cent. The math works because the volume is enormous and the labor is paid at, or below, local minimum wage.

The geographies are familiar to anyone who’s followed this story: the Philippines, Vietnam, Bangladesh, China, Indonesia, Egypt, Sri Lanka, Nepal, Venezuela, North Macedonia.

The Macedonian operation became famous in 2016, when over a hundred sites in the town of Veles outperformed the New York Times and the Washington Post combined on Facebook, on the twenty top-performing stories in the final three months of that year’s US presidential election. The operators were initially described as enterprising teenagers. They were later identified by OCCRP as a coordinated network run by a Macedonian media attorney named Trajche Arsov.

What changed between 2016 and now isn’t the rooms. It’s what gets typed into the phones.

The taps are still human. The words being tapped aren’t.

Click-farm operators have begun purchasing AI-generated text (post copy, comment templates, profile bios) to fill the content slot in their amplification pipeline. The amplification labor is still measured in human thumbs. The content being amplified is now produced at near-zero marginal cost by language models.

The 2024 Stanford Internet Observatory follow-up on the Macedonia networks documents the same operators, refined for the post-Twitter platform landscape, now running on AI-augmented content. The geography stayed the same. The tooling caught up.

Tier 2: The PR Firm With a Filing Number

SKDKnickerbocker LLC’s FARA filing, DOJ public record, August 29, 2025.

In August 2025, the Department of Justice posted a Foreign Agents Registration Act filing under the name SKDKnickerbocker LLC.

The filing reports a contract.

The contract is between SKDKnickerbocker, a US public-relations firm with offices in Washington, and the Israeli Ministry of Foreign Affairs. It runs from April 2025 to March 2026. The reported value is six hundred thousand dollars.

The filing describes the work. The strategy is called flooding the zone. The deliverables include the use of automated tools to amplify Ministry of Foreign Affairs messages on Instagram, TikTok, LinkedIn, and YouTube. There’s also coaching of on-camera spokespeople, journalist outreach, and influencer testing.

This is what coordinated amplification looks like when it shows up in the public legal record.

It has a budget line.

It has a registration number.

It has a brand-name firm with a website you can visit.

There’s one more thing in the public record that matters, and it’s the part most coverage of the SKDK filing has skipped.

SKDKnickerbocker is owned by a holding company called Stagwell. Stagwell also owns another PR firm called Targeted Victory. Targeted Victory has spent the same period running amplification campaigns for the other side of US political polarization.

Both firms subcontracted to the same French parent firm, Havas, on parallel pro-Israel work in 2025. Same parent. Two flavors. Bipartisan.

This is the part to sit with.

The bot infrastructure isn’t partisan. The bot infrastructure doesn’t pick a side. The bot infrastructure has a price list, and whichever client is paying that quarter is the side the infrastructure works for.

This is not a claim about whether the underlying client message is correct. This is a claim about what the filing documents.

A formal disclosure, a name-brand vendor, a six-figure contract, and a bipartisan parent company.

That’s the middle layer of the market. The labor layer hires people one at a time. The middle layer hires the labor layer.

Tier 3: The Subscription That Makes the Content

The middle layer needs people. The layer above it doesn’t.

In 2024, the Federal Trade Commission filed an action against a company called Rytr. Rytr sold a service that generated consumer reviews and testimonials at scale. The user picked a tone, picked keywords, picked a quantity, and got the reviews.

The FTC’s complaint said the service polluted the marketplace with a glut of fake reviews that consumers couldn’t distinguish from real ones.

The original order banned Rytr from selling review-generation services.

In December 2025, that order was reopened and set aside, following a Trump-administration directive to review AI-related FTC actions.

That sentence matters. Hold it for a second.

The case was settled. Then the case was unsettled. The regulatory posture toward the tier is itself in flux, and the firms operating in it know it.

The FTC has filed at least twelve AI-washing cases since 2024. The fourth one of 2025 was against a company called Air AI. The losses to small businesses in that case ran up to two hundred and fifty thousand dollars per claim.

The economics of this tier are different from the labor layer. There’s no labor cost. There’s no geographic constraint. A subscription buys you unlimited synthetic content output, and the marginal cost is whatever the AI inference call rounds to. Pennies.

This is the tier that broke the bottleneck.

It’s also the tier where the platform-tier story starts to fold back. The content the click farms now amplify is content the SaaS tools produced. The content the PR firms’ bot networks distribute is content the SaaS tools produced. The content that the next-layer-up platforms quietly monetize is, increasingly, content the SaaS tools produced.

The bottom of the stack got humans. The middle got firms. The top is about to get the venue.

Tier 4: The Platforms Don’t Want You to Notice

The top layer is the one nobody at the top layer wants to talk about, because it’s not a vendor. It’s the venue.

The Sherwood News report we opened with, the one about X paying creators to post AI-generated content, is the cleanest version. The platform’s revenue-share program incentivizes high-volume posting that meets engagement thresholds. The platform doesn’t check whether the engagement is from humans. The platform sells the impressions to advertisers, who pay against the engagement metric.

Inside that pricing model, the platform has no economic reason to distinguish a bot impression from a human impression. Until that changes, the platform has no incentive to remove either of them.

In October 2024, NBC News documented an AI-powered bot army on X spreading political content during the US election cycle. There was no central operator. The accounts behaved like a coordinated swarm in their outputs, but they were registered, paid, and operated through fragmented channels.

The market-size context is the part that quiets the room.

Before the numbers: these measure different things. Bot traffic, synthetic websites, paid engagement, and AI-generated posts are taken at different points in the funnel by different methodologies. What they share is a direction. The economic center of the internet is moving away from human attention and toward monetized signals that only sometimes correspond to it.

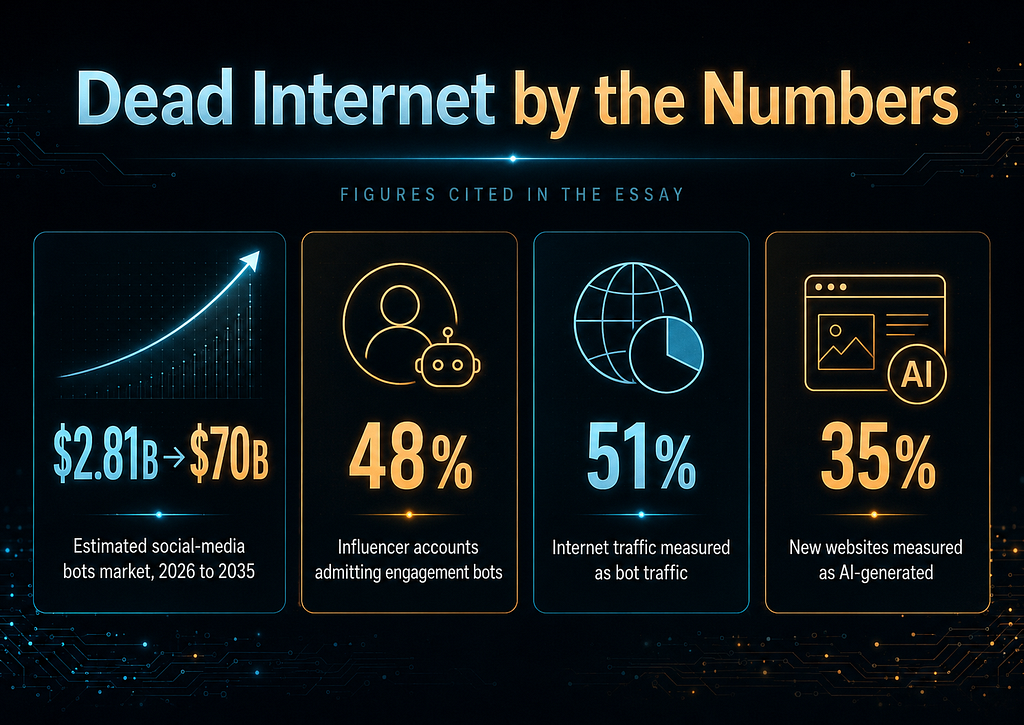

The social-media bots market was valued at $2.81 billion in 2026 and is projected to grow to $70 billion by 2035, at a compound annual growth rate of just under thirty-nine percent.

Forty-eight percent of influencer accounts in a 2025 industry survey admitted to using engagement bots.

In 2024, Imperva measured that fifty-one percent of all internet traffic came from bots.

In 2026, a joint study by Stanford, Imperial College, and the Internet Archive measured that thirty-five percent of all new websites were AI-generated.

There it is.

No one is running this.

Everyone is running this.

Three Things That Follow

If the four-tier framework is right, three things follow, and they’re uncomfortable in different ways.

First. Regulation doesn’t catch this. The EU’s AI Act, the FTC’s enforcement track, the state-level deepfake laws: each one is targeted at a single tier. None of them reach across the chain. A click farm in Vietnam buying content from a SaaS tool in San Francisco to amplify a payload commissioned by a PR firm in Washington for a sovereign client overseas is one operation, across four legal categories, across three jurisdictions. No regulator has clean jurisdiction over the whole chain.

The EU AI Act regulates Tier 3. The FTC enforces against Tier 3 (sometimes). FARA covers Tier 2. Nobody has jurisdiction over Tier 4 because Tier 4 is the platform that all three lower tiers run on, and the platform argues that what runs on it is speech.

Second. The incentive is monotonically pro-synthesis. Every tier wants next year to produce more synthetic engagement than this year. Platforms make more (higher ad prices on inflated metrics). SaaS sells more (rising synthetic-content demand pushes subscriptions). PR firms bill more (sovereign and corporate clients seeking amplification, and that demand never falls). Click farms scale more (labor-arbitrage opportunities continue, AI augmentation lifts productivity). There’s no actor inside the system with a reason to slow the system down.

This is why every “platform crackdown on bots” announcement reads as performative to anyone paying attention. The platform can’t afford to actually find the bots, because finding the bots reprices the inventory the platform is selling.

Third. The numbers you just saw, the 51% and the 35%, are old. The market is growing at thirteen to thirty-nine percent a year, depending on whose methodology you trust.

The synthetic share you experience today is higher than the most recent study can describe. By the time the 2027 numbers publish, the 2026 numbers will look quaint.

Who Has Standing to Stop the System?

The strong-version Dead Internet Theory imagines a single coordinating actor.

The four-tier framework shows the opposite. There’s no single actor because there doesn’t need to be one. The synthetic-engagement market is a thriving distributed economy in which each actor pursues their own profit and the aggregate outcome is the felt deadness of online life that viewers attribute, incorrectly, to a unified plan.

There’s no central conspiracy. There are many named, documented, financially-motivated actors at every tier. The system runs because there’s no central conspiracy. Decentralization is the architecture, not the mitigation.

Which leaves the question.

If every actor benefits, and no actor coordinates, then who has standing to stop the system?

The regulators are slower than the incentive structure they’re regulating. The platforms benefit from the same engagement metrics the bot operators are inflating. The AI labs producing the content acknowledge the problem and don’t own the consequence chain. The advertisers are paying for the engagement they say they want to clean up. And the readers: the people scrolling through the feed, the people writing real things into a comment section that’s mostly not real, the people running monetized accounts on platforms that quietly fund the slop that surrounds them.

Their own engagement contributes to the metric.

That’s the harder part.

The standing-to-stop problem isn’t that nobody could change this. It’s that everyone who could change it is currently being paid by it.

Including, in small ways, most of us. And knowing it.

That’s where this conversation has to go next. But before we get there, sit with what’s true now.

No one is running this.

Everyone is running this.

Sources:

- Jack Latham, Beggar’s Honey (2023): Vietnam click farms photojournalism

- OCCRP (2018), “The Secret Players Behind Macedonia’s Fake News Sites”: Arsov network investigation

- Stanford Internet Observatory (2024): Macedonia tactical evolution follow-up

- Sludge (September 15, 2025), “Democratic PR Firm to Run Bot Army for Israel”: SKDK case

- FARA filings, DOJ (August 29, 2025): SKDKnickerbocker LLC registration

- FTC press releases: Rytr (2024), Air AI (August 2025), Workado (2025)

- Sherwood News (2025), Elon Musk + X bots coverage

- NBC News (October 2024), AI-powered bot army on X investigation

- Business Research Insights (2026), Social Media Bots Market sizing

- Stanford / Imperial / Internet Archive (2026), 35% AI-generated new sites

- Imperva (2024), 51% bot traffic measurement