The $75 billion IPO looked like a triumph. Read the S-1 and you find something more complicated.

On June 12, 2026, SpaceX began trading on the Nasdaq under the ticker SPCX at $135 per share. By the closing bell, shares had gained 19% to $160.95. By June 15, they were trading at $177.99. The company raised $85.7 billion when underwriters exercised their overallotment option, making it the largest public offering in stock market history, nearly three times Saudi Aramco’s prior record of $29.4 billion in 2019.

And somewhere in that math, Elon Musk became the world’s first trillionaire.

His SpaceX stake (roughly 42% of a company now valued at over $2 trillion) is worth approximately $840 billion on its own. Add his Tesla position, his X (formerly Twitter) holding, and the xAI assets folded into SpaceX in February 2026, and you cross $1 trillion before you run out of items on the list. The milestone is real. It happened during the three days SPCX has been publicly traded.

But the bigger story isn’t that one person became worth $1 trillion. It’s how the deal was structured — and what that structure means for everyone who bought in at $135.

The Number That Doesn’t Make Sense

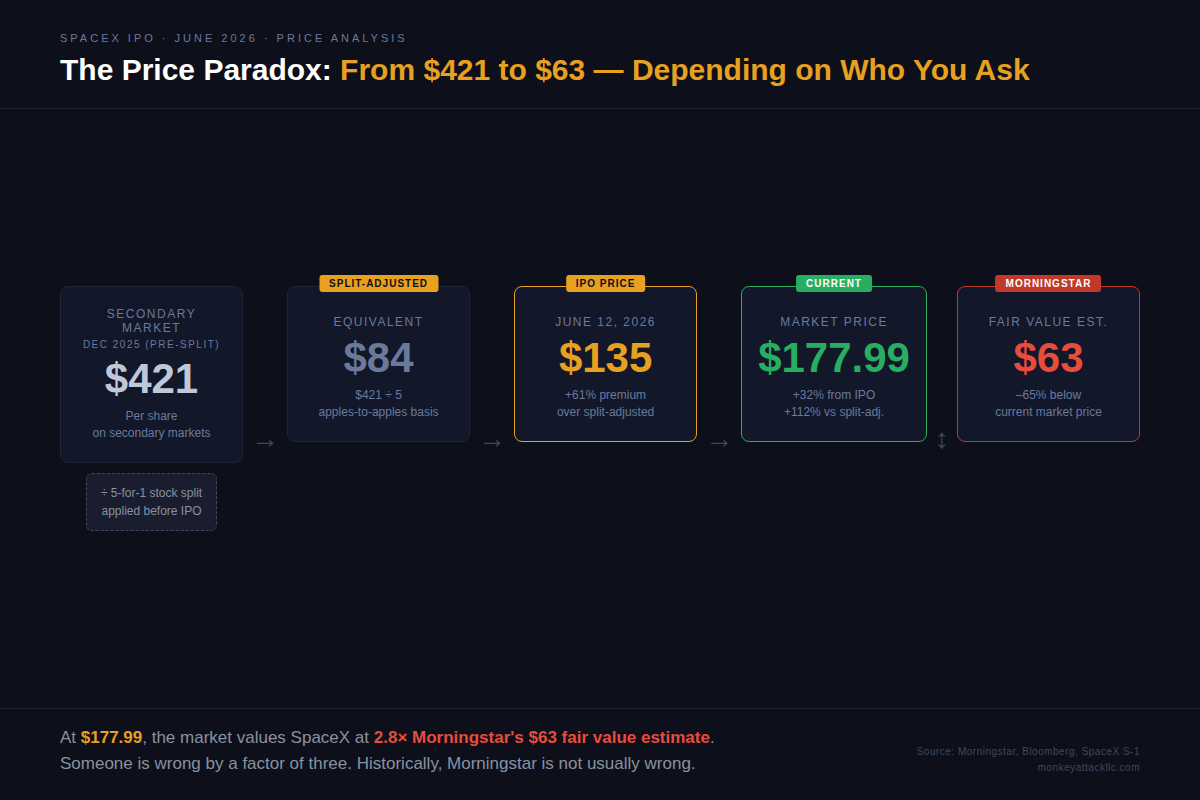

Private market investors were paying $421 per share for SpaceX in December 2025. Accredited investors on Hiive, one of the secondary trading platforms, were posting bids above $600 per share as recently as April 2026. The IPO priced at $135.

This isn’t a typo. SpaceX executed a 5-for-1 stock split in May 2026, which converts those private market prices: $421 becomes roughly $84 post-split, $600 becomes $120. So the $135 IPO price does represent a modest premium to the last official insider transaction, but the secondary market premium that had been building for years was essentially erased on IPO day.

Who captured that spread? The employees and early investors who held original shares, now converting at IPO. The public, buying at $135, got in after the 32x run from SpaceX’s 2015 Series F, not alongside it.

What You Actually Bought

SpaceX’s 2025 financials, per the S-1: $18.7 billion in revenue (+43% year-over-year), a net loss of $4.94 billion. Morningstar pegged the fair value at $63 per share, a 53% discount to the IPO price. Morningstar is famously conservative on growth names, and SpaceX’s trajectory arguably justifies a premium. But the gap between $63 and $135 is large enough that it warrants acknowledgment.

What’s driving the growth story is Starlink. The satellite internet division generated $11.4 billion in 2025 (61% of total revenue), with operating profit of $4.4 billion. Subscriber count crossed 10 million in February 2026. The growth rate is real. The launch business adds strategic depth and government contract revenue that insulates SpaceX from commercial market cycles. These are genuine assets.

The February 2026 acquisition of xAI, the AI company Elon Musk founded, added another layer. SpaceX absorbed xAI in an all-stock deal that CNBC called the largest corporate merger in history. Combined value at closing: approximately $1.25 trillion. Public investors who bought SPCX on June 12 now own exposure to Grok, xAI’s AI model, and the AI compute infrastructure xAI had been building. Whether that’s a feature or a complication depends on your view of AI-to-SpaceX synergies, which the S-1 describes but doesn’t quantify.

The Governance Structure Nobody Wants to Talk About Loudly

Here is the part that prompted a letter from the Council of Institutional Investors dated June 9, 2026, three days before trading began, and an analysis from Harvard Law’s corporate governance blog titled “Top IPO, Weak Governance.”

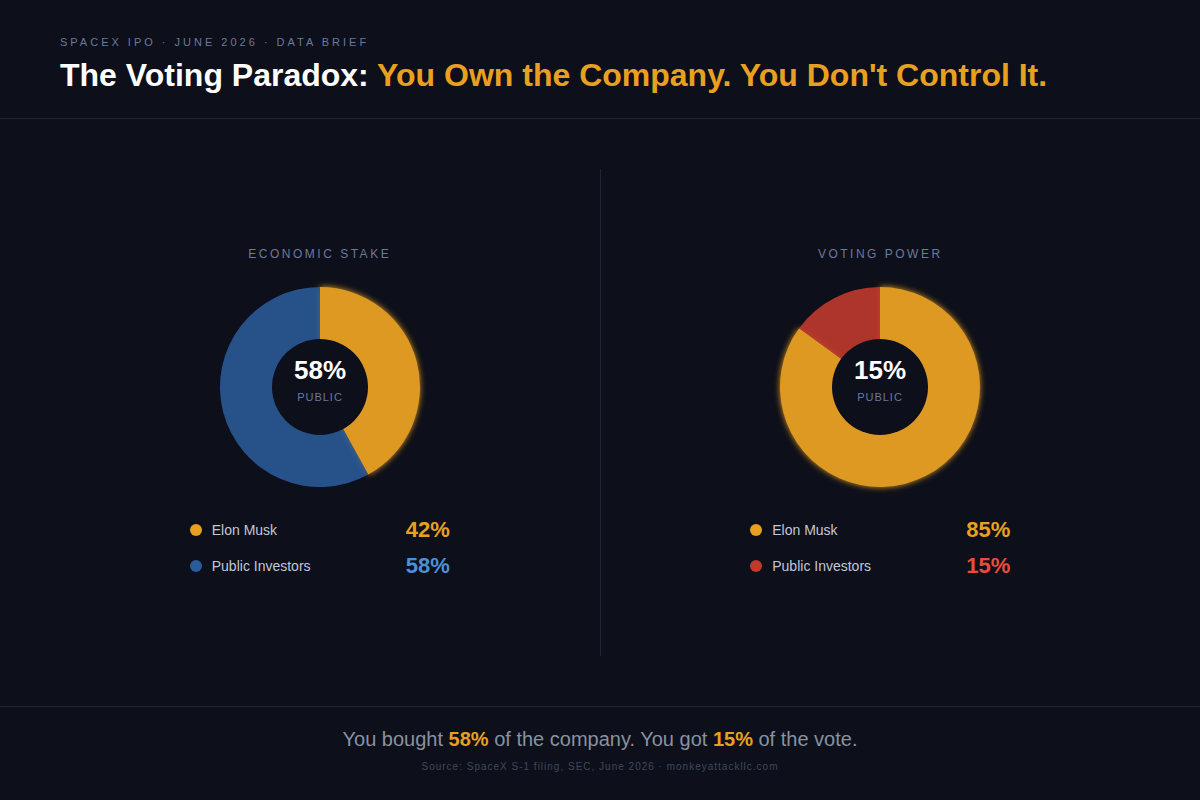

SpaceX has two classes of common stock. Class A shares, the ones the public bought at $135, carry 1 vote each. Class B shares, held almost entirely by Elon Musk (93.6% of all outstanding Class B), carry 10 votes each. The result: Musk holds 42% of the economic interest in SpaceX and approximately 85% of the voting power.

The practical consequence of this math: Elon Musk cannot be removed as CEO of SpaceX. The only mechanism for removing him requires a majority vote of Class B shareholders. Since Musk holds 93.6% of Class B, triggering that mechanism requires his own vote in favor of his own removal. He is, in the most literal structural sense, irremovable.

SpaceX has classified itself as a “controlled company” under Texas law, which exempts it from requirements for a majority-independent board and from independent nominating and compensation committees. This isn’t unusual for founder-controlled companies (Google, Meta, and Snap have similar structures), but those companies went public earlier in their lifecycle. SpaceX raised $85 billion from the public at a $1.75 trillion valuation while maintaining a governance structure that offers public shareholders essentially no say in how the company is run.

One additional provision received almost no coverage in the pre-IPO press: the corporate opportunities clause. SpaceX’s charter grants board members, including members who simultaneously serve on Tesla, the Boring Company, Neuralink, and xAI boards, the legal right to redirect business opportunities from SpaceX to those other companies. This clause is standard in complex corporate groups, but the scope of Musk’s simultaneous leadership positions makes it structurally significant. A board member who sits on both the SpaceX and Tesla boards can legally offer a technology licensing opportunity to Tesla first. The S-1 discloses this. Public investors accepted it when they bought the stock.

The X/Tesla/DOGE Entanglement

Musk’s simultaneous leadership of SpaceX, Tesla, X (formerly Twitter), xAI (now merged into SpaceX), the Boring Company, Neuralink, and his role heading the Department of Government Efficiency (DOGE) during the Trump administration creates a web of potential conflicts that the S-1 lists as risk factors but cannot resolve.

SpaceX’s single largest customer is the U.S. federal government, specifically NASA and the Department of Defense. The question of whether Musk’s proximity to government decision-making as head of DOGE influenced the volume or pricing of SpaceX’s government contracts is not one the S-1 answers. It is listed as a risk factor. It may become a legal question eventually. It remains unresolved.

Tesla and SpaceX share manufacturing supply chains, engineering talent pools, and, through the xAI merger, AI infrastructure investments. X provides the communications platform on which Musk routinely makes statements that move markets, including SpaceX-adjacent markets. The corporate opportunities clause discussed above means the connections between these entities are not just reputational or relational; they are legally permitted.

Public shareholders bought into this structure knowingly. The S-1 is public record. The governance terms were published three weeks before the IPO priced. Demand was 4x oversubscribed anyway.

The Investors Who Won

Founders Fund, Peter Thiel’s venture vehicle, invested approximately $600 million in SpaceX across 20-plus years. At the IPO price and valuation, that stake is worth north of $50 billion, roughly an 80x return.

Ontario Teachers’ Pension Plan invested approximately $300 million in 2019, the first deployment of their newly-created venture growth arm. That position is now worth approximately $11.6 billion, a 38x return in seven years.

Google and Fidelity both participated in SpaceX’s $1 billion Series F in 2015 at a $10-12 billion valuation. Their combined stake, estimated at approximately 6-7% of SpaceX at the time, is worth somewhere in the range of $100-150 billion today, depending on exact dilution. A $900 million Google check became a position worth an estimated $120 billion.

For context: those are the people on the other side of the public float. The $135 IPO price is what retail and institutional investors paid after those returns had already been realized.

The Part That Is Genuinely Extraordinary

None of the above changes the underlying fact: SpaceX has built something that was widely considered impossible twenty years ago.

Reusable orbital rockets. A satellite internet constellation serving over 10 million customers across every inhabited continent. The only non-government vehicles currently capable of crewed orbital flight. Starship, the most powerful rocket ever built, now flying. A serious, funded, technically-progressing program to put humans on Mars.

Those numbers are in the S-1: $18.7 billion in revenue, 43% year-over-year growth, $4.4 billion in Starlink operating profit. The company has achieved positive cash flow from operations while simultaneously funding some of the most capital-intensive infrastructure in human history.

What makes this IPO genuinely historic is not just the size or the valuation. It’s that the company selling shares is demonstrably attempting something that has never been done: building a multi-planetary human civilization, funded by a satellite internet business and a launch services monopoly.

The governance structure may be weak, the valuation stretched, the conflicts of interest permanent. Morningstar may still be right that the fair value is half the IPO price.

But SpaceX is also the company running humanity’s best current bet on reaching Mars.

The S-1 disclosed every word of it. Investors bought it anyway. And on June 12, 2026, they collectively made Elon Musk the first trillionaire in human history while doing it.

History tends to look generous on people who bought into transformational infrastructure early, even when the price was high and the governance was weak. Whether this is that moment, or whether Morningstar’s $63 number eventually proves prophetic, is the only question that matters now. The answer won’t arrive for years.

SPCX is currently trading at $177.99. The S-1 is available on SEC EDGAR. Form your own view.